Eltoma Corporate Services — Authorised Corporate Services Provider

Articles are provided for general informational purposes by an authorised corporate services provider and do not constitute legal advice.

Cyprus remains a relevant European jurisdiction for inbound business, holding, financing, intellectual property and regional operating structures. However, the Cyprus corporate tax analysis should no longer be presented simply by reference to the historical 12.5% corporation tax rate. For contemporary advisory work, and particularly after the 2026 reform, the question is wider: how does the whole tax, compliance and substance profile of the structure operate?

For business owners, investors and entrepreneurs from third countries, including Russia, Ukraine, China and other non-EU jurisdictions, the Cyprus company is often expected to support several objectives at the same time: European market access, family or founder relocation, banking, group management, intellectual property, financing, trading and tax residence planning. The tax architecture must therefore be assessed as a combined framework rather than as a single rate.

The principal recent amendment is the increase of the Cyprus corporate income tax rate from 12.5% to 15% with effect from 1 January 2026. Official Cyprus material identifies the new rate as applying to Cyprus tax-resident companies and permanent establishments within the Cyprus charge. Older references to 12.5% should therefore be treated with caution when preparing contemporary models, client memoranda, tax projections or website materials. [1]

The increase does not remove Cyprus from the range of competitive EU corporate jurisdictions. It does, however, change the commercial arithmetic. A trading company, a finance company, an IP company, a holding company or a regional coordination vehicle should now be modelled on the 15% baseline, subject to the availability of any exemptions, deductions, incentives or treaty outcomes that are properly supported by the facts.

The reform should also be read together with the more developed anti-avoidance and transparency environment. In particular, 2026 materials refer to low-tax jurisdiction screening, while Tax Department announcements confirm DAC8 developments in April 2026. The practical result is that inbound structures should be analysed not only by reference to tax payable in Cyprus, but also by reference to how the structure will be reported, exchanged, disclosed and viewed by other tax administrations.

The Cyprus corporate income tax framework applies to Cyprus tax-resident companies and to permanent establishments within the Cyprus charge. Company residence should not be reduced to incorporation alone. The domestic Cyprus approach continues to focus on management and control, which makes governance evidence central to any residence analysis.

In practice, advisers should examine where board-level and strategic decisions are actually taken, whether Cyprus resident directors perform real decision-making functions, where risks are controlled, where contracts are approved and whether the company records support the asserted position. A Cyprus registered office, nominee administration or routine corporate secretarial presence is not, by itself, a complete tax-residence analysis.

Permanent establishment exposure should be kept distinct from residence. A foreign enterprise may remain non-resident at company level and still create a Cyprus taxable presence through local premises, employees, dependent agents, recurring contract-concluding activity or other factual arrangements. This is particularly relevant where a foreign group relocates founders, senior managers, sales staff, technical teams or operational personnel to Cyprus.

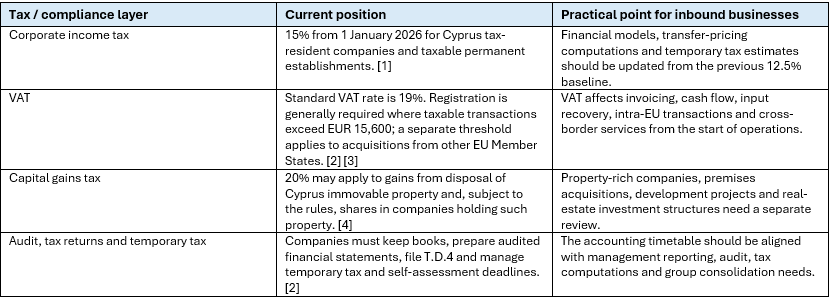

Cyprus corporate tax compliance is not merely an annual filing exercise. Official business-registration guidance states that legal entities must register through the Tax For All portal, keep books and records, prepare audited financial statements through an approved auditor, submit the company income tax return using Form T.D.4, submit temporary tax in two instalments on 31 July and 31 December, and complete the self-assessment payment process by 1 August of the following year.

For inbound businesses, these obligations should be built into the implementation timetable from the beginning. Weak bookkeeping, delayed management accounts, unmodelled temporary tax, incomplete invoicing and late audit preparation can create practical tax risk even where the underlying structure is technically sound.

This is particularly important for foreign-owned Cyprus companies that expect to open bank accounts, pass compliance reviews, obtain audit sign-off, support substance evidence or demonstrate that Cyprus management is real. The accounting record becomes part of the evidential architecture of the tax position.

The following table summarises the principal recurring tax and compliance layers that should be considered at the structuring stage. The table is deliberately not a substitute for detailed advice; it is intended to show why Cyprus corporate tax planning cannot be reduced to corporation tax alone.

VAT is often the most immediate operational tax for a newly established Cyprus business. It affects pricing, contracts, invoicing systems, cash flow, input recovery and whether the company can evidence that it is carrying on taxable activity in Cyprus. For consultancy, e-commerce, trading, software, logistics, real estate and cross-border service businesses, VAT should be reviewed before the first invoice is issued, not after the first quarter has closed.

Capital gains tax is narrower in scope but can be commercially significant where Cyprus immovable property is involved. The Cyprus Tax Department refers to a 20% charge on gains from the disposal of immovable property situated in Cyprus and shares of companies holding such property, subject to the applicable rules. For many inbound investors, the Cyprus company may hold office premises, development assets or local property-linked investments. That factual feature can move the analysis beyond ordinary corporate income tax.

The increase to a 15% corporation tax rate does not remove the relevance of Cyprus tax incentives. Official Ministry of Finance materials continue to refer to the Notional Interest Deduction on qualifying new equity and the nexus-based IP regime, including the 80% exemption for qualifying IP income. The Tax Department also continues to refer to tax benefits from reorganisations.

These features remain important for equity-funded groups, IP-rich businesses and restructuring projects. However, they should not be presented as isolated benefits. NID analysis depends on new equity, taxable profits and the assets financed by that equity. IP treatment depends on the nexus approach and the relationship between development activity, ownership, income and expenditure. Reorganisation relief requires careful legal and tax classification.

Critical analysis is therefore required. The 2026 rate increase may make deductions and incentives more valuable in arithmetic terms, but the same development also strengthens the need for evidence. A tax incentive should be supported by legal documentation, accounting treatment, transfer-pricing analysis and a commercial rationale proportionate to the company’s actual role.

Cyprus transfer pricing should be treated as part of the normal corporate tax architecture for foreign-owned companies. The Tax Department’s transfer-pricing materials link Cyprus practice to Article 33 of the Income Tax Law and the OECD Transfer Pricing Guidelines. Controlled transactions should therefore be identified, categorised, measured and documented by reference to arm’s-length principles.

This is especially important for inbound groups using Cyprus companies for management services, financing, procurement, licensing, cost sharing, treasury, holding activities or regional coordination. A service agreement, loan agreement or IP licence between related parties is not merely a legal document; it is also a transfer-pricing fact pattern.

Current official materials also refer to Cyprus Local File and Summary Information Table requirements and to threshold consequences where controlled transactions in relevant categories exceed the applicable annual threshold. Back-to-back financing and other recurring related-party arrangements should not be supported by a one-off benchmark that is left untouched. The facts, functions, risks and pricing should be reviewed on a periodic and, where necessary, annual basis.

Cyprus continues to have a substantial treaty network, and the Tax Department publishes the list and text of double tax agreements. Treaty access remains an important part of Cyprus structuring, particularly for holding, finance and royalty flows.

However, the simplified statement that Cyprus is a zero-withholding jurisdiction is no longer a sufficiently safe professional formulation. Contemporary advice should consider treaty residence, beneficial ownership, commercial rationale, substance, anti-avoidance and low-tax-jurisdiction screening. Official materials for 2026 identify low-tax jurisdictions for the tax year under Circular 1/2026, and reform materials refer to measures concerning outbound dividend, interest and royalty payments to low-tax jurisdictions.

The practical implication is clear. Where a Cyprus company pays dividends, interest or royalties into a low-tax or high-risk ownership chain, advisers should not stop at domestic withholding language. The payment should be tested by jurisdiction, recipient status, beneficial ownership, treaty entitlement, commercial purpose and evidence of real functions in Cyprus.

Substance is relevant across the whole tax architecture. It supports company residence, treaty access, beneficial ownership, transfer pricing, permanent establishment analysis, banking due diligence and audit evidence. It also protects against the professional risk of presenting a Cyprus company as something that the facts do not support.

The level of substance required will depend on the function performed. A passive holding company, finance company, IP company, trading company and operating headquarters will not require identical personnel, premises, decision-making or risk-control arrangements. However, each structure should be capable of explaining why the Cyprus company exists, what functions it performs, what risks it assumes and how its accounts reflect that position.

For founders and mobile entrepreneurs, this point should be connected with immigration, payroll and personal tax residence planning. If the founder is physically relocating to Cyprus, the company’s management, employment and tax position should be aligned with the residence route, remuneration, social insurance and bank onboarding evidence. Separating those workstreams may create avoidable inconsistencies.

Cyprus corporate tax planning now sits within a broad transparency architecture. The Tax Department’s official materials refer to automatic exchange and reporting systems including FATCA, CRS, country-by-country reporting, DAC6 and DAC7. In 2026, DAC8 was added to this environment through announcements concerning the entry into force of the Administrative Cooperation in the Field of Taxation (Amending) Law of 2026.

This development is relevant not only to regulated or crypto-asset businesses. It reflects the general direction of tax administration: structures are increasingly visible across borders. For inbound groups, the question is therefore not only how the Cyprus company is taxed, but also how the structure, ownership chain, cross-border payments, reporting obligations and related-party transactions will appear in exchange-of-information systems.

The most common risk is using an outdated Cyprus model. A structure that was designed by reference to 12.5% corporation tax, simple treaty assumptions and limited substance may require revision after the 2026 reform and related anti-avoidance developments.

Other recurring risks include incorporating before deciding where management and control will genuinely be exercised; relocating personnel without testing permanent establishment exposure; failing to register for VAT on time; treating temporary tax as a post-year-end issue; entering related-party loans or service arrangements without transfer-pricing support; assuming treaty benefits without beneficial ownership and substance; making outbound payments without low-tax-jurisdiction screening; and ignoring capital gains tax where Cyprus immovable property is involved.

For business owners and investors, the practical lesson is that Cyprus implementation should be integrated. Corporate, tax, accounting, payroll, immigration, banking and audit considerations should be reviewed together rather than as separate administrative tasks.

Cyprus remains a technically useful EU jurisdiction for inbound businesses, holding structures, financing arrangements, IP projects and regional operations. The 15% corporate income tax rate remains competitive in an EU context, and the jurisdiction continues to offer a treaty network, recognised incentives and a familiar common-law corporate environment.

The post-2026 analysis is nevertheless more demanding. The rate increase, transfer-pricing framework, low-tax-jurisdiction measures, VAT and capital gains exposure, reporting architecture and substance requirements mean that Cyprus should be assessed as a serious EU corporate platform, not as a simple low-rate incorporation venue.

From 1 January 2026, the Cyprus corporate income tax baseline used in the article is 15% for Cyprus tax-resident companies and taxable permanent establishments. Older 12.5% references should be checked before being used in financial models or client memoranda.

Cyprus may remain attractive as an EU corporate platform, but the analysis should not be limited to the headline rate. Advisers should examine residence, management and control, VAT, incentives, treaty access, transfer pricing, substance, banking and reporting obligations.

Incorporation is relevant, but a proper Cyprus corporate tax analysis also considers management and control, decision-making, directors' functions, contractual approvals, risk control and supporting records.

VAT registration should be assessed before trading starts. Official Business in Cyprus guidance refers to a EUR 15,600 taxable-transaction threshold and separate rules for acquisitions from other EU Member States. The factual position and intended activities should be checked before invoicing begins.

Foreign-owned Cyprus companies commonly enter into related-party service, financing, licensing, procurement or management arrangements. These should be identified and documented under arm's-length principles by reference to Article 33 and OECD transfer-pricing guidance.

That shorthand is no longer sufficiently precise for professional materials. Outbound dividend, interest and royalty flows should be checked against domestic law, treaty access, beneficial ownership, substance, anti-avoidance rules and low-tax-jurisdiction screening.

The main risk is treating incorporation, tax, accounting, VAT, payroll, banking and transfer pricing as separate administrative tasks. For a defensible structure, those workstreams should be aligned from the first accounting period.

The article should contain direct answer paragraphs, clear H2 headings, a source-backed professional summary, visible FAQ content and JSON-LD Article and Breadcrumb List schema. FAQ schema may be included as optional semantic markup, subject to Google feature availability.

Articles are provided for general informational purposes by an authorised corporate services provider and do not constitute legal advice.

Receive updates with practical insights on international business, law, tax, accounting, and compliance.

Be the first to hear about our latest discounts and special offers!

Follow our Telegram channel for offshore industry news:

Want updates by e-mail?

Enter your email address below to subscribe to our newsletter!