Eltoma Corporate Services — Authorised Corporate Services Provider

Articles are provided for general informational purposes by an authorised corporate services provider and do not constitute legal advice.

Cyprus remains one of the most attractive European jurisdictions for entrepreneurs, investors, family offices, internationally mobile executives and high-net-worth individuals. A central feature of the Cyprus personal tax system is the non-domicile regime, under which qualifying Cyprus tax resident individuals who are not domiciled in Cyprus are generally exempt from Special Defence Contribution on dividend and interest income.

Following the 2026 Cyprus tax reform and Tax Circular 02/2026 issued by the Cyprus Tax Department on 29 May 2026, Cyprus introduced an alternative method for the imposition of Special Defence Contribution on dividend and interest income for certain individuals. The new method allows eligible individuals to elect for a fixed Special Defence Contribution liability by paying €250,000 for a five-year period, subject to approval by the Tax Commissioner.

The measure is especially relevant to individuals who do not have a Cyprus domicile of origin but who are expected to become deemed domiciled in Cyprus under the 17-out-of-20-year rule. For such individuals, the new regime may operate as a planning tool that provides certainty and, in appropriate cases, a material reduction in SDC exposure on substantial dividend and interest income.

This article explains the current Cyprus Special Defence Contribution regime, how it applies to domiciled and non-domiciled individuals, how the 17-out-of-20-year deemed domicile rule works, how the new fixed-payment method operates, and the practical calculations that should be reviewed before making an election.

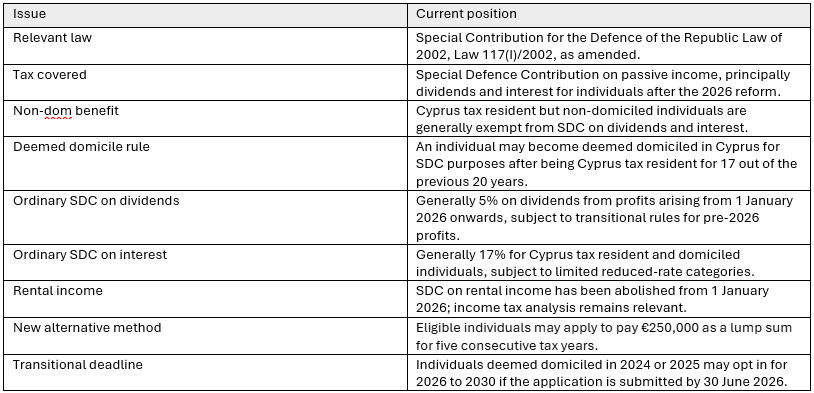

Special Defence Contribution, commonly referred to as SDC, is a Cyprus tax imposed under the Special Contribution for the Defence of the Republic Law of 2002, Law 117(I)/2002, as amended. The Cyprus Tax Department describes SDC as a contribution imposed in accordance with that law on prescribed types of income.

For individuals, SDC is particularly relevant to passive income. Historically, this included dividends, interest and rental income. Following the 2026 tax reform, the practical SDC focus for individuals is now primarily on dividend income and interest income. Rental income is no longer subject to SDC from 1 January 2026, although it may still be subject to ordinary income tax depending on the facts.

SDC must be distinguished from ordinary Cyprus income tax. Dividend income and certain interest income may be exempt from ordinary income tax, but may still be subject to SDC if the individual is both Cyprus tax resident and domiciled in Cyprus.

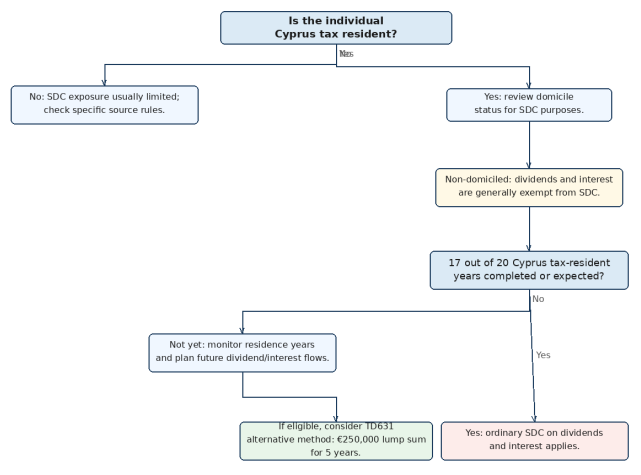

The SDC analysis for individuals is a two-stage exercise. First, it is necessary to determine whether the individual is Cyprus tax resident under the Income Tax Law of 2002, Law 118(I)/2002, as amended. Secondly, it is necessary to determine whether the individual is domiciled in Cyprus for SDC purposes under the Special Contribution for the Defence of the Republic Law of 2002, Law 117(I)/2002, as amended, and the principles of domicile under the Wills and Succession Law, Cap. 195.

This distinction is critical. A person may be Cyprus tax resident but non-domiciled in Cyprus. In that case, the individual is generally exempt from SDC on dividends and interest. By contrast, a Cyprus tax resident individual who is domiciled or deemed domiciled in Cyprus is generally within the ordinary SDC regime.

An individual may be Cyprus tax resident under the ordinary 183-day rule where the individual is physically present in Cyprus for more than 183 days in the relevant tax year. Cyprus also has a 60-day tax residence route for individuals who satisfy the statutory conditions, including a sufficient physical presence in Cyprus and a genuine connection with Cyprus.

The statutory tax residence rules are contained in Article 2 of the Income Tax Law of 2002, Law 118(I)/2002, as amended. A detailed day-count and supporting documentation review is recommended before treating an individual as Cyprus tax resident, particularly where the individual has connections with more than one jurisdiction.

The Cyprus non-dom regime is one of the main attractions of the Cyprus personal tax system. A Cyprus tax resident individual who is not domiciled in Cyprus is generally exempt from SDC on worldwide dividend income and interest income.

For a foreign-origin individual relocating to Cyprus, the practical result can be significant. An individual may become Cyprus tax resident and still remain non-domiciled for SDC purposes. During that period, dividends and interest may fall outside SDC, subject to separate analysis of General Healthcare System contributions, foreign withholding tax and any other applicable tax rules.

The concept of domicile is based on domicile of origin and domicile of choice. Domicile of origin is generally acquired at birth. Domicile of choice may be acquired by establishing a home in a jurisdiction with the intention of permanent or indefinite residence. For SDC purposes, Article 2(3) of the Special Contribution for the Defence of the Republic Law of 2002, Law 117(I)/2002, as amended, is the key provision to review.

The Cyprus non-dom benefit is not indefinite. An individual who has been Cyprus tax resident for at least 17 out of the 20 years immediately before the relevant tax year may be deemed domiciled in Cyprus for SDC purposes, regardless of domicile of origin.

This rule is the main trigger for the new alternative fixed-payment method. A foreign-origin individual may have enjoyed the SDC exemption for many years as a Cyprus tax resident non-dom. Once the 17-out-of-20-year threshold is reached, the individual may become subject to ordinary SDC on dividends and interest unless a specific exemption applies or the new alternative method is elected.

For long-term residents, it is therefore important to maintain an accurate tax residence history. The analysis is not limited to the current year. It requires a review of the previous 20 tax years and the number of years in which the individual was Cyprus tax resident.

Once an individual becomes domiciled or deemed domiciled in Cyprus, the ordinary SDC regime becomes relevant. For dividends from profits arising from 1 January 2026 onwards, the ordinary SDC rate for Cyprus tax resident and domiciled individuals is generally 5%. For interest income, the ordinary SDC rate is generally 17%, subject to limited reduced-rate categories.

Transitional rules remain important for dividends from pre-2026 profits. A dividend paid in 2026 is not automatically subject to the 5% rate merely because it is paid in 2026. It is necessary to identify the profit pool from which the dividend is paid. Dividends from profits arising before 1 January 2026 may remain subject to the previous 17% SDC rate in certain circumstances.

Tax Circular 02/2026 introduced an alternative method for the imposition of SDC on dividend and interest income for certain eligible individuals. The Cyprus Tax Department has also published Form TD631, the application form for individuals electing to be subject to the alternative method of imposing SDC.

Under the alternative method, an eligible individual may apply to the Tax Commissioner to pay a fixed amount of €250,000 for a five-year period. This represents €50,000 per year, but it is paid as a lump sum. Once the application is approved and the payment is made, the individual is subject to the alternative method for the relevant five-year period instead of being taxed under the ordinary SDC rules on actual dividend and interest income.

The regime is designed to provide certainty and, in appropriate cases, reduce the SDC cost for individuals with substantial dividend or interest income. It is not a general personal tax exemption and does not remove other Cyprus or foreign tax obligations.

The alternative method is targeted at individuals who do not have a Cyprus domicile of origin and who are expected to become domiciled in Cyprus under the 17-out-of-20-year rule. It is therefore not a general election available to all Cyprus tax residents.

The regime is most likely to be relevant to long-term foreign-origin Cyprus tax residents who have substantial dividend or interest income and who are approaching the point at which their SDC non-dom protection would otherwise cease.

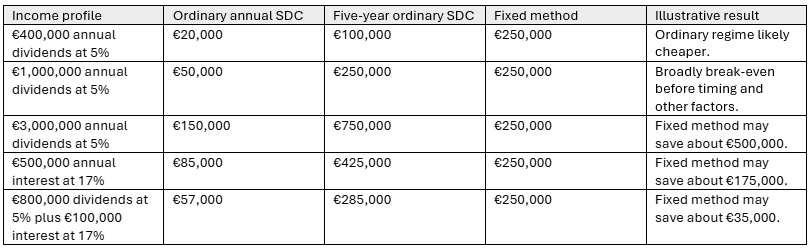

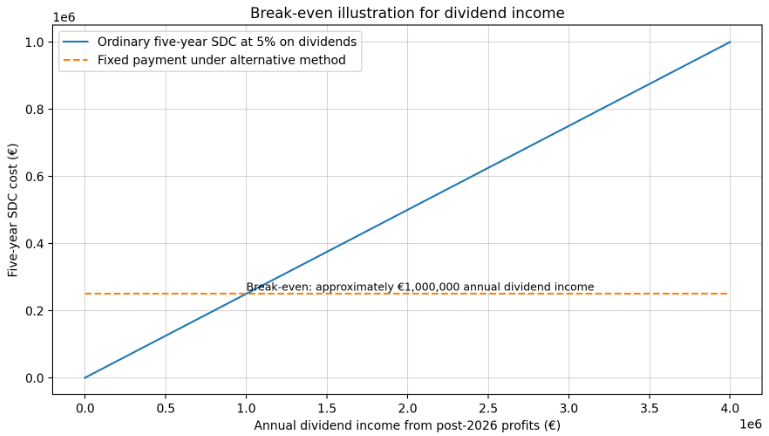

In commercial terms, the regime is potentially attractive where the individual expects that ordinary SDC on dividends and interest over five years would exceed €250,000.

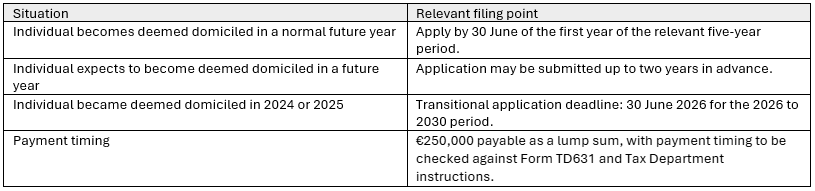

The general application deadline is 30 June of the first year of the relevant five-year period. The circular wording also provides that an individual may submit the application up to two years in advance of the year in which the individual is expected to become domiciled in Cyprus.

The Cyprus Tax Department Form TD631 indicates that the €250,000 SDC amount for the entire five-year period is payable by the end of the month following the month in which the application is made. This timing point is important for liquidity planning.

Transitional provisions apply for individuals who became domiciled in Cyprus in the 2024 or 2025 tax years. Such individuals may opt into the alternative regime for the period 2026 to 2030, provided that their application is submitted by 30 June 2026.

The commercial analysis is straightforward in principle. The taxpayer should compare the expected ordinary SDC liability for the five-year period with the fixed payment of €250,000.

The break-even point is an ordinary SDC liability of €50,000 per year. If the individual expects to pay less than €50,000 per year under the ordinary rules, the fixed method may be more expensive. If the individual expects to pay more than €50,000 per year, the fixed method may be advantageous.

For dividend income alone, assuming the 5% SDC rate applies, the approximate break-even point is €1,000,000 of annual dividend income. For interest income alone, assuming the 17% SDC rate applies, the approximate break-even point is €294,118 of annual interest income.

Figure 2: Simplified break-even illustration for dividend income from post-2026 profits.

Example 1: an individual becomes deemed domiciled in Cyprus in 2026 and expects to receive annual dividends of €3,000,000 from profits arising after 1 January 2026. Under the ordinary regime, SDC at 5% would be €150,000 per year. Over five years, the ordinary SDC cost would be €750,000. If the individual qualifies for the alternative method and pays €250,000, the potential SDC saving would be approximately €500,000.

Example 2: an individual expects to receive annual dividends of only €400,000 from post-2026 profits. The ordinary SDC at 5% would be €20,000 per year, or €100,000 over five years. In that case, the fixed payment of €250,000 would generally be more expensive.

Example 3: an individual expects significant interest income of €500,000 per year. At the ordinary 17% SDC rate, the annual SDC would be €85,000, or €425,000 over five years. In that scenario, the fixed method may be commercially attractive, subject to eligibility and the wider tax analysis.

Example 4: an individual became deemed domiciled in 2025. The transitional rules may allow the individual to apply for the fixed method for 2026 to 2030, but the application must be submitted by 30 June 2026. Missing the deadline may remove the opportunity for that five-year period.

The alternative method applies to SDC on dividends and interest. It should not be treated as a complete personal tax exemption. A taxpayer considering the election should separately review Cyprus income tax, General Healthcare System contributions, foreign withholding tax, foreign tax residence, double tax treaty issues, reporting obligations and banking compliance.

The election also does not replace the need to analyse the company profit pool. Where dividends are paid from pre-2026 profits, transitional SDC rules may be relevant. Where value is transferred to shareholders in a non-dividend form, disguised dividend rules should be considered.

The new regime is relevant not only to individuals but also to Cyprus companies, holding structures and family office arrangements with individual shareholders. A Cyprus holding company may have accumulated profits from different years. If the ultimate shareholder has historically been non-domiciled but is about to become deemed domiciled, future dividend planning should be reviewed carefully.

Companies should identify retained earnings by tax year, assess whether 2024 or 2025 transitional deemed dividend distribution rules remain relevant, review the timing of dividend declarations, and ensure that shareholder domicile declarations and tax residence information are up to date.

For owner-managed companies, additional attention should be given to shareholder loans, use of company property, asset transfers and arrangements that may be treated as disguised dividends.

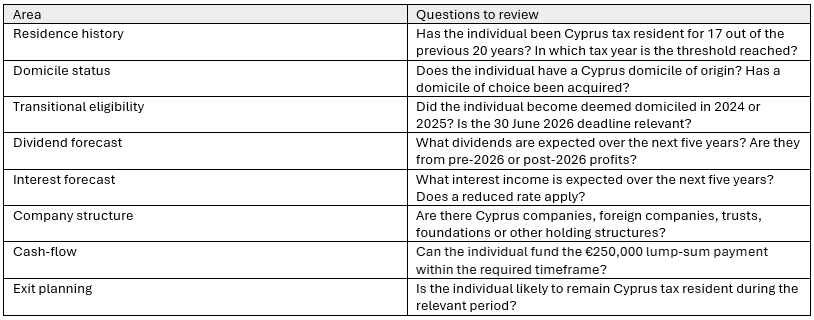

Before applying for the alternative method, the individual should carry out a structured review. The election may be financially beneficial in the right case, but it should not be made automatically.

Cyprus companies with individual shareholders should also review the SDC impact of the 2026 reform. The relevant analysis is not limited to the individual’s personal return. It may affect dividend planning, shareholder documentation and corporate governance.

The 2026 alternative fixed-payment method is a significant development for long-term Cyprus non-domiciled individuals. It provides a mechanism for eligible individuals to pay €250,000 for a five-year period instead of paying SDC on actual dividend and interest income.

The regime is likely to be attractive where the individual expects substantial dividends or interest and where ordinary SDC over five years would exceed €250,000. It is unlikely to be attractive where income is modest, uncertain or unlikely to be distributed during the relevant period.

For individuals who became deemed domiciled in 2024 or 2025, the transitional deadline of 30 June 2026 is particularly important. Such individuals should urgently review their position and determine whether an application is commercially justified.

Eltoma Global can assist with Cyprus tax residence and domicile reviews, SDC exposure calculations, Cyprus company profit pool analysis, dividend planning and preparation of the relevant supporting materials for the alternative method application.

Special Defence Contribution is a Cyprus tax imposed under the Special Contribution for the Defence of the Republic Law of 2002, Law 117(I)/2002, as amended. For individuals, it is mainly relevant to dividend and interest income after the 2026 reform.

For individuals, SDC generally applies where the individual is both Cyprus tax resident and domiciled or deemed domiciled in Cyprus. Cyprus tax resident but non-domiciled individuals are generally exempt from SDC on dividends and interest.

The Cyprus non-dom exemption generally allows Cyprus tax resident individuals who are not domiciled in Cyprus to receive dividend and interest income without SDC.

An individual may be deemed domiciled in Cyprus for SDC purposes if he or she has been Cyprus tax resident for at least 17 out of the previous 20 years.

The alternative method allows eligible individuals to apply to pay a lump sum of €250,000 for a five-year period instead of paying SDC on actual dividend and interest income.

The regime is aimed at individuals who do not have a Cyprus domicile of origin and who are expected to become, or have recently become, deemed domiciled in Cyprus under the 17-out-of-20-year rule.

The general deadline is 30 June of the first year of the relevant five-year period. Transitional cases for individuals deemed domiciled in 2024 or 2025 must be reviewed urgently because the stated deadline is 30 June 2026.

No. It is mainly beneficial where the ordinary SDC liability over five years would exceed €250,000. If expected dividend and interest income is modest, the ordinary regime may be cheaper.

No. It concerns SDC on dividends and interest. Cyprus income tax, General Healthcare System contributions, foreign tax, reporting obligations and other issues must be reviewed separately.

Articles are provided for general informational purposes by an authorised corporate services provider and do not constitute legal advice.

Receive updates with practical insights on international business, law, tax, accounting, and compliance.

Be the first to hear about our latest discounts and special offers!

Follow our Telegram channel for offshore industry news:

Want updates by e-mail?

Enter your email address below to subscribe to our newsletter!