Eltoma Corporate Services — Authorised Corporate Services Provider

Articles are provided for general informational purposes by an authorised corporate services provider and do not constitute legal advice.

Greece remains a significant EU relocation jurisdiction for third-country nationals seeking residence access, family mobility and a European base for personal or business planning. The Greek Golden Visa programme, formally structured as an investor residence route, continues to be available. However, the programme has changed materially following the 2024 amendments to the Greek Migration Code.

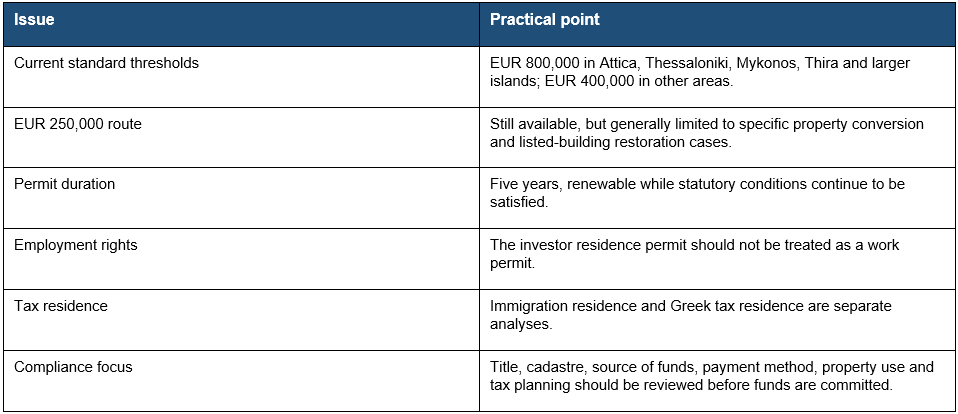

For most new real estate investments, Greece should no longer be described as a general EUR 250,000 Golden Visa jurisdiction. The standard property route is now largely structured around higher location-based thresholds, with EUR 250,000 retained only for specific statutory categories, principally certain conversion-to-residential-use and listed-building restoration cases.

The current framework should therefore be considered not merely as an immigration product, but as part of a wider relocation analysis covering property acquisition, source of funds, banking, tax residence, corporate structuring, bookkeeping, VAT, payroll and operational presence in Greece.

The relevant legislative framework is the Greek Migration Code, Law 5038/2023, which the Ministry of Migration and Asylum confirmed as entering into force on 31 March 2024. The real estate investor route is now contained in Article 100 of Law 5038/2023, as replaced by Article 64 of Law 5100/2024. The statutory framework refers to investments in immovable property, a permanent investor residence permit and residence permit type B.5.

The permit is granted for five years and may be renewed, provided that the statutory conditions continue to be satisfied. The route applies to qualifying third-country nationals who have lawfully entered or lawfully reside in Greece and who acquire qualifying immovable property, either directly or, in certain circumstances, through a legal entity established in Greece or another EU Member State, where the applicant wholly holds the relevant shares or corporate interests.

Official Ministry materials identify the principal application and renewal documentation, including application form, passport photographs, certified travel document, fee evidence, insurance, notarial certificate, land registry or cadastre evidence and property-specific supporting documents. In practice, this means that the legal and documentary preparation should begin before the applicant is commercially committed to a particular property.

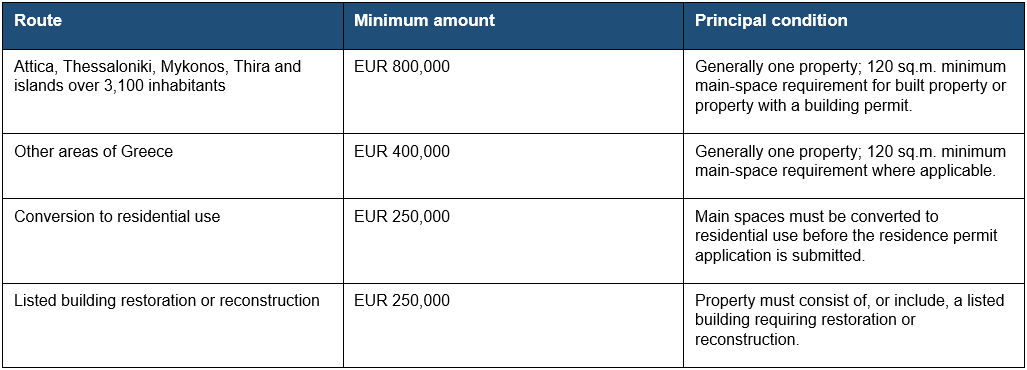

The 2024 reform introduced a more restrictive and location-sensitive structure. For the Region of Attica, the Regional Unit of Thessaloniki, the Regional Units of Mykonos and Thira, and islands with a population exceeding 3,100 inhabitants according to the latest census, the minimum acquisition value is EUR 800,000. The investment must generally be made in one property and, for built property or property with a building permit, the main spaces must be at least 120 square metres.

For the remaining areas of Greece, the minimum acquisition value is EUR 400,000. The same one-property and 120 square metre requirements apply where relevant. The result is a materially higher entry cost for most standard real estate acquisitions, particularly in Athens, Thessaloniki, Mykonos, Santorini and larger islands.

The EUR 250,000 level has not been abolished, but it is now confined to specific statutory categories. It should not be presented as the general market-entry threshold for new investors.

The first category concerns investment in immovable property whose main spaces are changed to residential use. The provision also covers certain industrial buildings, or parts of industrial buildings, provided that no industry has been installed and operating there for at least the preceding five years. The change of use must be completed before the residence permit application is submitted.

The second category concerns the purchase of immovable property consisting of a listed building, or part of a listed building, requiring restoration or reconstruction. The investment must be made in one property, and transfer of the property before full restoration or reconstruction is completed is invalid under the relevant provision.

These reduced-threshold routes require technical legal and planning due diligence. Advisers should review zoning, change of use, technical certificates, restoration obligations, timing, contractual protections, title, cadastre status and practical completion risk before a client commits funds.

The agreed price or rent must be paid in full before submission of the application. The legislation specifies permitted payment methods, including crossed bank cheque, credit transfer and POS payment through a payment service provider operating in Greece. Details of payment and the parties must be declared before the notary and recorded in the relevant deed.

For renewal, the investor must continue to hold the property or maintain the qualifying contract and the other statutory conditions must continue to be met. Article 100 also provides that periods of absence from Greece do not constitute an impediment to renewal of the investor residence permit.

A key compliance restriction concerns property use. Properties acquired for the initial grant or renewal of the investor permit may not be leased on a short-term basis within the sharing-economy framework and may not be subleased. In addition, properties acquired under the EUR 250,000 conversion-to-residential-use route may not be used as the registered seat or branch of a business. Breach may lead to revocation of the residence permit and an administrative fine of EUR 50,000. Certain listed-building restoration and prohibited-transfer breaches may attract a EUR 150,000 fine.

The 2024 reform included transitional provisions. Existing investor residence permits granted under the previous rules remain in force and may be renewed if the conditions applicable at the time of grant continue to be satisfied.

Certain investors were permitted to complete under the previous regime by 31 December 2024, provided that specified steps had been taken by 31 August 2024. These steps included payment of a 10% deposit, payment of the agreed price or rent, signing of a notarial preliminary agreement, or signing of a private agreement of specified date supported by banking evidence. If the original acquisition was not completed, a further qualifying investment could be completed under the previous conditions, but not beyond 30 April 2025.

For new investors, the current thresholds should be assumed unless a verified transitional position applies. Advisers should not rely on transitional treatment without reviewing the relevant contractual date, payment evidence, notarial documentation and current administrative position.

The Golden Visa provides a residence basis in Greece for qualifying investors and supports personal relocation planning. It also sits within the Schengen environment. EU materials describe short stays in the Schengen area by reference to the 90 days in any 180-day period rule. A Greek residence permit supports lawful residence in Greece, but should not be treated as unrestricted residence rights in all other Schengen states.

The investor permit is not an employment permit. Article 100 expressly states that residence permits granted under that article do not establish a right of access to any form of work. Business owners should therefore distinguish carefully between passive investment, residence planning, remote management of non-Greek business interests, local employment, establishment of a Greek company and the creation of Greek taxable presence or permanent establishment risk.

At EU level, investor residence schemes remain subject to scrutiny. The European Commission has identified risks connected with security, money laundering, tax evasion and corruption, and has emphasised the need for transparency, effective oversight and proper checks around such schemes.

At Greek level, the Golden Visa reforms sit alongside wider legal migration changes. Law 5275/2026 implements Directive (EU) 2024/1233 on a single application procedure for a single residence and work permit for third-country nationals and also amends the Migration Code. The Ministry of Migration and Asylum has presented the 2026 reforms as part of a modernised legal migration framework intended to reduce bureaucracy, accelerate procedures and respond to labour-market needs.

Immigration residence and tax residence are separate questions. The Greek Independent Authority for Public Revenue explains that tax residence determines the state entitled to tax an individual on worldwide income. Under Article 4 of the Greek Income Tax Code, an individual may be treated as Greek tax resident if they have their permanent or principal residence, habitual abode or centre of vital interests in Greece, or if they are present in Greece for more than 183 days cumulatively during any 12-month period, subject to specific exceptions.

Accordingly, a Golden Visa does not itself answer whether an individual becomes Greek tax resident, whether a foreign company may become managed from Greece, whether payroll or social security obligations arise, whether a Greek company should be incorporated, or whether Greek bookkeeping, VAT, corporate tax and reporting obligations may be triggered.

Before committing to an investment, advisers should confirm the applicant’s nationality, family composition, intended days of presence in Greece, business role, ownership structure, source of funds, banking access, property use, tax residence position and whether a Greek operating company is required.

The Greek Golden Visa remains a relevant residence-planning route for third-country nationals, particularly for internationally mobile families, investors and business owners considering Greece as a personal or strategic base. However, the 2024 reforms have materially changed the programme’s cost, compliance and planning profile.

The standard real estate route is now structured around EUR 800,000 and EUR 400,000 thresholds, with the EUR 250,000 level retained only for specific conversion and listed-building cases. The programme also includes stricter restrictions on short-term letting, subleasing and certain business uses of qualifying property.

For legal, tax and business advisers, the appropriate question is not simply whether a client can obtain a Greek Golden Visa. The more complete analysis is whether the Golden Visa is the correct residence route within a wider Greek relocation plan, taking into account immigration status, tax residence, property compliance, corporate structuring, banking, source-of-funds review and the client’s intended personal and commercial presence in Greece.

The Greece Golden Visa is an investor residence route for qualifying third-country nationals. The real estate route is contained in Article 100 of Law 5038/2023, as replaced by Article 64 of Law 5100/2024, and provides a five-year renewable investor residence permit where the statutory conditions continue to be met.

For Attica, Thessaloniki, Mykonos, Thira and islands with more than 3,100 inhabitants, the principal real estate threshold is EUR 800,000. For other areas of Greece, the principal threshold is EUR 400,000. In both cases, the investment is generally in one property and built property or property with a building permit must satisfy a 120 square metre main-space requirement.

Yes, but it is no longer the general market-entry route. The EUR 250,000 threshold is retained for specific cases, principally qualifying properties whose main spaces are converted to residential use and certain listed buildings requiring restoration or reconstruction.

Properties acquired for the initial grant or renewal of the investor permit may not be leased on a short-term basis within the sharing-economy framework and may not be subleased. Breach may lead to permit revocation and administrative fines.

The investor residence permit should not be treated as an employment permit. Article 100 provides that residence permits granted under that article do not establish a right of access to any form of work.

No. A Greek residence permit supports lawful residence in Greece. It may facilitate Schengen mobility, but it should not be treated as an unrestricted right to live or work in other Schengen states.

Not by itself. Immigration residence and tax residence are separate questions. Greek tax residence depends on Article 4 of the Greek Income Tax Code, including permanent or principal residence, habitual abode, centre of vital interests and the 183-day rule.

Advisers should review the applicant’s nationality, family composition, property threshold, title, cadastre status, source of funds, permitted payment method, property use, tax residence, business role, family planning, banking access and whether a Greek operating company or other local obligations may arise.

Articles are provided for general informational purposes by an authorised corporate services provider and do not constitute legal advice.

Receive updates with practical insights on international business, law, tax, accounting, and compliance.

Be the first to hear about our latest discounts and special offers!

Follow our Telegram channel for offshore industry news:

Want updates by e-mail?

Enter your email address below to subscribe to our newsletter!