Eltoma Corporate Services — Authorised Corporate Services Provider

Articles are provided for general informational purposes by an authorised corporate services provider and do not constitute legal advice.

Hong Kong and Singapore remain two of Asia’s most important corporate structuring centres. Both jurisdictions are attractive to founders, investors, international groups, family offices and professional advisers because they combine commercial efficiency with sophisticated legal infrastructure. The same features, however, also require a disciplined regulatory perimeter for those who form companies, provide registered office services, arrange nominee roles, deal with beneficial ownership information or assist with corporate administration.

For licence holders and professional firms, the practical question is not whether they describe themselves as a “corporate services” provider. The more important question is whether the substance of the activity falls within a regulated service category. A business may present its service as administration, coordination, introduction, accounting support or investor structuring. That label will not be decisive if the activity in fact involves company formation, officer arrangements, nominee services, address services, trust-related services, designated accounting-service activities or official filings.

This article compares the Hong Kong Trust or Company Service Provider regime and the Singapore Corporate Service Provider regime from the perspective of a licence holder or regulated professional firm. It focuses on what is regulated, what is not regulated in the same way, and which boundary issues should be reviewed before providing services in practice.

The Hong Kong and Singapore regimes share a common policy background: the prevention of money laundering, terrorism financing and misuse of legal entities. They are, however, structured differently.

In Hong Kong, the relevant framework is the TCSP licensing regime administered by the Companies Registry under the Anti-Money Laundering and Counter-Terrorist Financing Ordinance. A person who carries on, or wishes to carry on, a trust or company service business in Hong Kong is required to apply for a TCSP licence. The official Hong Kong guideline identifies the regime as applying to individuals, partnerships and corporations that intend to provide trust or company services in Hong Kong and to those already granted a TCSP licence. [1]

In Singapore, the relevant framework is the CSP regime under the Corporate Service Providers Act 2024 and related regulations. ACRA states that, from 9 June 2025, all corporate service providers must register with ACRA, comply with new obligations and vet nominee directors. ACRA has also stated that all business entities carrying on a business of providing corporate services in and from Singapore must register as registered CSPs and comply with AML, counter-proliferation-financing and counter-terrorism-financing obligations. [2] [3]

The difference is important. Hong Kong is framed around the business of providing trust or company services in Hong Kong. Singapore is framed around the business of providing specified corporate services in and from Singapore, including some activities that will be particularly relevant to accounting, tax and filing practices.

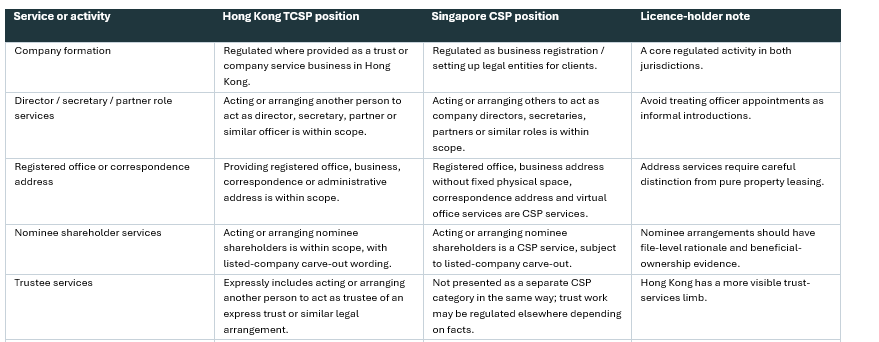

In Hong Kong, the principal trigger is the carrying on of a trust or company service business in Hong Kong. The services captured include forming corporations or other legal persons; acting, or arranging for another person to act, as director, secretary, partner or in a similar position; providing registered office, business, correspondence or administrative address services; acting or arranging for another person to act as trustee of an express trust or similar legal arrangement; and acting or arranging for another person to act as nominee shareholder, subject to the listed-securities carve-out. [4]

In Singapore, ACRA’s registration guidance states that a person must register as a CSP if it provides any of six categories of services to others: business registration, address services, role services, nominee shareholder services, designated accounting services and filing services. [5] This makes the Singapore perimeter particularly operational. It does not merely capture incorporation and nominee activity; it also expressly captures certain filing and accounting-related service lines.

From a licence-holder perspective, the first compliance step should therefore be a written service-perimeter analysis. The question should not be “what do we call our service?”, but rather “what do we actually do for the client?”

There is substantial overlap between the two jurisdictions. Company formation is regulated in both systems. Acting as, or arranging for another person to act as, a director, secretary, partner or similar officer is also within scope. Address services and nominee shareholder arrangements are likewise core regulated activities.

This overlap matters because many business owners experience these services as one bundled engagement: incorporation, registered office, company secretary, initial filings, nominee assistance and annual maintenance. For a provider, however, each component may have its own regulatory significance. A firm may be outside the perimeter for one activity but inside it for another. Conversely, a professional exemption may remove the need for a TCSP licence in Hong Kong, but it does not remove AML and record-keeping duties where those duties apply under the professional regime.

The most obvious distinguishing feature of the Hong Kong TCSP regime is the express trust-services limb. The definition of trust or company service business includes acting, or arranging for another person to act, as trustee of an express trust or similar legal arrangement. This is commercially relevant in private wealth, family office, holding company and asset-protection structures. Where a firm’s corporate services are connected to trust administration, trustee appointment or nominee shareholder arrangements, Hong Kong perimeter analysis should be undertaken with particular care.

Hong Kong also contains important exemptions. The official guideline states that the TCSP licensing requirement, including the fit and proper test, does not apply to the Government, authorised institutions, certain licensed corporations where the TCSP business is ancillary, accounting professionals, legal professionals and prescribed classes of persons.

However, exemption from applying for a licence to the Registrar should not be misunderstood as an absence of regulation. The Hong Kong guideline states, for example, that certain accounting and legal professionals that carry on trust or company service business may not need to apply for a licence from the Registrar, but remain subject to the regulatory regime of the relevant professional regulator and the AMLO requirements relating to customer due diligence and record-keeping.]

Accordingly, the Hong Kong analysis is often a two-stage exercise. First, is the activity within the trust or company service business definition? Secondly, if it is within the definition, does the provider require a TCSP licence, or is it exempt but still regulated through a professional AML framework?

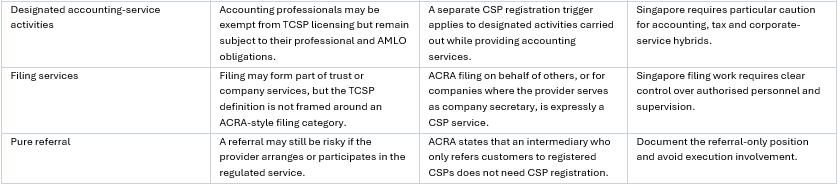

Singapore’s CSP regime has several features that require particular attention from professional firms. First, ACRA’s guidance expressly includes designated accounting services. It states that CSP registration is required where a provider carries out transactions for customers while providing accounting services for designated activities. The accounting services identified include financial accounting, internal audit, management accounting and taxation services. The designated activities include buying or selling real estate, managing customer money, securities or assets, managing bank, savings or securities accounts, organising contributions for creating, operating or managing corporations, creating, operating or managing legal persons or legal arrangements, and buying and selling business entities. [8]

This is significant for accounting and tax practices. A firm that considers itself to be outside company secretarial work may still need to review whether its accounting or tax service line includes a designated activity. The risk is particularly acute where accounting support is combined with transaction execution, management of client assets, management of accounts, corporate restructuring support or the creation and management of entities.

Secondly, Singapore treats filing services as an express CSP category. ACRA’s guidance covers filing ACRA transactions on behalf of others and filing for companies where the provider serves as company secretary. This makes internal control over filing authority, registered qualified individuals and authorised staff practically important.

Thirdly, nominee-director controls are a major feature of the Singapore reforms. ACRA states that persons acting as nominee directors by way of business are prohibited unless the appointments are arranged by registered CSPs and the persons have been assessed as fit and proper by those CSPs. ACRA also notes that a registered CSP must not arrange a person to act as nominee director unless it is satisfied that the person is fit and proper.

The commercial conclusion is clear: in Singapore, the regulated perimeter should be tested not only against incorporation and address services, but also against filings, accounting-service activities and nominee-director arrangements.

Address services are regulated in both jurisdictions, but the practical boundary is not always obvious. In Hong Kong, the TCSP definition includes providing a registered office, business address, correspondence address or administrative address for a corporation, partnership or other legal person or legal arrangement. [4] In Singapore, ACRA’s guidance identifies registered office addresses, business addresses without fixed physical space, correspondence addresses where customers can be contacted but are not physically present, and virtual office services as CSP address services. [5]

The important distinction is between an address service and an ordinary property arrangement. ACRA states that a landlord who leases a dedicated physical unit or space to a business that uses it as its registered office, business or correspondence address under a proper tenancy agreement does not need CSP registration. [11] That exclusion should not be stretched too far. A virtual office, mail-forwarding or registered office service provided to multiple clients is a different risk profile from leasing a dedicated office under a genuine tenancy agreement.

Licence holders should be precise when using the expression “outside scope”. It can mean several different things.

First, an activity may be genuinely outside the TCSP or CSP perimeter. For example, pure legal or tax advice that does not involve formation, officer arrangements, nominee services, address services, designated accounting activities or filings may not itself be a TCSP/CSP service. Secondly, an activity may be exempt from the TCSP licensing requirement in Hong Kong because it is performed by an exempt professional or institution, but it may still be subject to AML, customer due diligence and record-keeping requirements under another regime. Thirdly, an activity may be outside Singapore CSP registration because it is only a referral to a registered CSP, a dedicated premises lease, or filing for one’s own entity or related group entities in the capacities identified by ACRA. [11]

The safest wording is therefore not “unregulated”. It is: “outside the TCSP/CSP registration perimeter, subject to other applicable laws and professional obligations.” This distinction is more accurate and reduces the risk of giving clients a false sense that no compliance requirements apply.

Several grey areas deserve particular attention. Bundled engagements: incorporation, address services, company secretary, nominee support and annual filings are often sold together but may need to be analysed separately. Informal introductions: introducing a person who may act as director, nominee shareholder or address provider can become regulated if the firm is effectively arranging the role or billing for that arrangement. Accounting and tax hybrids: in Singapore, the addition of designated accounting-service activities can change the regulatory analysis for a professional firm that does not present itself as a corporate secretarial provider. Cross-border delivery: a provider should analyse where the business is carried on, from where services are delivered, and which jurisdictional registration or licensing trigger is engaged.

Reliance on exemptions: exemptions should be documented with reasons, not assumed from professional title or firm description.

Prepare a service-perimeter memorandum for Hong Kong and Singapore separately. Map every service line against the statutory categories, including bundled and ancillary services. Separate regulated services, exempt services, referral-only services and services provided by another licensed or registered provider. Review website descriptions and engagement letters to ensure they do not overstate or obscure the actual service performed. Document reliance on any exemption or carve-out. Maintain registers for nominee, address, incorporation, filing and designated accounting-service activities where applicable.

Train staff not to arrange nominee or officer roles informally without approval. Review cross-border delivery models, especially where Hong Kong and Singapore teams jointly service the same client group.

Hong Kong and Singapore both regulate corporate-service activity, but they do not do so through identical perimeter rules. Hong Kong’s TCSP framework is particularly important for trust and company services, nominee shareholder arrangements, address services and the professional exemption analysis. Singapore’s CSP framework is particularly important for the expanded corporate-services perimeter, designated accounting-service activities, ACRA filing services and nominee-director controls.

For licence holders, the correct approach is substance-led. A firm should examine what is actually being done, who performs it, where it is performed, whether the client pays for the service, and whether the activity falls into a statutory category. Descriptions such as “consultancy”, “administration”, “coordination” or “support” should not be allowed to obscure the regulatory analysis.

For business owners and investors, the practical lesson is equally clear. Using a properly licensed, registered or exempt professional provider is not merely a compliance formality. It supports bankability, corporate credibility, beneficial-ownership transparency and reputational risk management in two of Asia’s most important business jurisdictions.

Hong Kong focuses on the business of providing trust or company services in Hong Kong, while Singapore’s CSP regime is framed around specified corporate services provided in and from Singapore, including filing services and designated accounting-service activities.

Yes. Company formation is a core regulated activity in both regimes when provided as a business to clients. The licensing or registration analysis should be undertaken before offering incorporation packages.

Yes. Hong Kong includes registered office, business, correspondence and administrative address services within the TCSP perimeter. Singapore also treats registered office, business address, correspondence address and virtual office services as CSP address services, subject to specific exclusions such as genuine dedicated premises leasing.

A pure referral may be outside scope, especially in Singapore where ACRA identifies referral-only intermediaries as not requiring CSP registration. However, the position changes if the firm arranges, executes, controls or bills for the regulated service.

Singapore expressly includes designated accounting services where a provider carries out specified customer transactions while providing accounting services. This may affect accounting, taxation and corporate-service hybrid practices even where they do not present themselves as company secretarial providers.

No. An exemption from applying for a Hong Kong TCSP licence does not necessarily remove AML, record-keeping or professional regulatory obligations. The more accurate position is that the activity may be outside the TCSP/CSP registration perimeter, subject to other applicable laws and professional obligations.

Articles are provided for general informational purposes by an authorised corporate services provider and do not constitute legal advice.

Receive updates with practical insights on international business, law, tax, accounting, and compliance.

Be the first to hear about our latest discounts and special offers!

Follow our Telegram channel for offshore industry news:

Want updates by e-mail?

Enter your email address below to subscribe to our newsletter!