Eltoma Corporate Services — Authorised Corporate Services Provider

Articles are provided for general informational purposes by an authorised corporate services provider and do not constitute legal advice.

In case 2C_506/2024 of 4 May 2026, the Swiss Federal Supreme Court addressed an important question for international tax practice: whether correspondence between a taxpayer’s lawyers and a domestic Swiss tax authority could be withheld from transmission to a foreign tax authority on the basis of attorney-client privilege or professional secrecy. The Court rejected the taxpayer’s position and permitted the transmission of the correspondence in the context of international tax administrative assistance.

The decision is commercially significant because tax residence disputes, treaty-benefit claims, substance reviews and cross-border structuring enquiries are increasingly determined by documentary evidence. A taxpayer may hold a formal tax residence certificate in one jurisdiction, yet another jurisdiction may seek to test whether that certificate reflects the factual reality. In that evidential exercise, the administrative file held by the first jurisdiction can become important.

For legal, tax, accounting and corporate-service professionals, the decision is a useful reminder that communications strategy is not a secondary administrative issue. It is an essential part of cross-border tax risk management. When counsel writes to an authority, the correspondence should be drafted on the assumption that it may later be reviewed by a foreign tax authority, a court or another competent body under an information-exchange mechanism.

The case arose from a request made by the Spanish tax authority to the Swiss Federal Tax Administration. Spain was examining whether an individual who claimed Swiss tax residence was, in substance, tax resident in Spain. In order to substantiate that enquiry, the Spanish authority sought information including tax residence certificates issued by the competent Swiss cantonal authority and correspondence exchanged between that authority and the taxpayer’s lawyers.

The taxpayer objected to the disclosure of the lawyer-authority correspondence and argued that it was protected by attorney-client privilege. That argument required the Court to distinguish between confidential communications within the lawyer-client relationship and correspondence which, although prepared or sent by lawyers, had been submitted to a public authority and retained within that authority’s file.

The Supreme Court dismissed the appeal. The decision is reported as intended for publication and is notable because it clarifies the treatment of lawyer-authority correspondence held by the domestic tax authority in the specific context of international tax administrative assistance.

The central issue was not whether a taxpayer may obtain privileged legal advice. That proposition remains orthodox. The issue was narrower and more practical: does the protection extend to correspondence between the taxpayer’s legal counsel and the tax authority, once that correspondence is held by the authority and forms part of the administrative record?

The Court’s answer was, in substance, no. The protective rationale of legal professional secrecy is to preserve the confidentiality of legal advice, litigation strategy and communications between lawyer and client. It does not automatically convert all documents prepared by a lawyer into permanently privileged material, particularly where those documents have deliberately been communicated to a public authority in the course of an administrative process.

This distinction is critical. Internal advice, draft analysis, confidential memoranda and instructions between client and counsel should be treated separately from letters, submissions, forms and explanatory documents sent to the tax authority. The former may remain within the protected lawyer-client sphere. The latter may become part of the administrative file.

Swiss international administrative assistance in tax matters forms part of the broader international architecture for the exchange of tax information. The Swiss Federal Tax Administration explains that administrative assistance is used for the exchange of information between tax authorities and is based on double taxation agreements, tax information exchange agreements and the Multilateral Convention on Mutual Administrative Assistance in Tax Matters. Exchange of information upon request is commonly governed by the applicable double taxation agreement and by Swiss domestic procedural rules, including the Tax Administrative Assistance Act.

The Swiss Federal Tax Administration also notes that a foreign authority may request different categories of information in order to clarify a taxpayer’s tax position. Examples include banking information, information concerning Swiss companies and personal information, including data relevant to tax residence. The present decision should therefore be seen against a procedural framework that is designed to enable tax authorities to exchange information where the relevant treaty and domestic-law requirements are met.

The practical question for advisers is not whether Switzerland participates in tax transparency mechanisms. It does. The more relevant question is how a taxpayer’s documentary record will appear if it is transmitted to another jurisdiction. That question becomes particularly sensitive where the documents concern residence, management, beneficial ownership, treaty entitlement or economic substance.

The decision should not be overstated. It does not abolish attorney-client privilege, nor does it mean that a foreign authority may obtain a lawyer’s entire file merely because the lawyer has acted for the taxpayer in a tax matter. The privileged sphere remains highly important and should be carefully preserved.

As a working distinction, the protected category will normally include confidential advice given by counsel to the client, internal legal analysis, strategic memoranda, draft advice, correspondence between client and lawyer and other materials that have not been submitted to a third party. These documents are the substance of the advisory relationship and are distinct from the administrative record maintained by the tax authority.

However, where lawyers make submissions to an authority, apply for residence certificates, correspond with a tax office, submit factual explanations or seek administrative confirmation, those communications may be treated as dealings with the authority rather than as confidential lawyer-client advice. The adviser’s professional status does not, by itself, shield the document once it has entered the authority’s file.

The decision is particularly relevant to tax residence disputes involving internationally mobile individuals. Such disputes are rarely determined by a single document. A tax residence certificate may be highly relevant, but it is not necessarily conclusive if another jurisdiction has factual grounds to examine the taxpayer’s centre of life, home, family connections, business activity, travel pattern, banking activity or economic interests.

In practice, a foreign tax authority may seek to compare the formal position asserted in one jurisdiction with the factual evidence available in another. Correspondence with the Swiss tax authority may therefore be used to test the basis on which a residence certificate was issued, what facts were represented to the authority and whether those representations are consistent with the taxpayer’s wider conduct.

For business owners, founders and investors, this is an important planning point. Relocation to a new jurisdiction should not be treated as a purely formal exercise involving immigration status, a local lease and a residence certificate. It should be accompanied by a coherent factual record that supports the intended tax position. The tax, legal, accounting, immigration, banking and corporate documents should all tell the same story.

Although the case concerned individual tax residence, its practical implications extend to companies and holding structures. Cross-border corporate tax disputes frequently involve questions of place of effective management, permanent establishment, beneficial ownership, treaty access, economic substance and the commercial rationale for a particular structure. In each of these areas, the evidential record is decisive.

A company may have constitutional documents, board minutes, accounting records and service agreements in one jurisdiction, while its beneficial owners, directors or key decision-makers are located elsewhere. If the company or its advisers have corresponded with a domestic tax authority in support of a particular position, that correspondence may later become relevant to another jurisdiction’s enquiry.

Owner-managed businesses are particularly exposed to this risk. The distinction between the individual’s residence position and the company’s management position may be blurred where the same individual is a shareholder, director, signatory, investor and operational decision-maker. For such clients, correspondence with authorities should be reviewed not only for its immediate purpose, but also for its possible collateral use in future cross-border enquiries.

The decision is especially relevant for internationally mobile clients from third countries, including business owners and investors from Russia, Ukraine, China and other jurisdictions who relocate their personal residence, move family wealth, establish holding structures or use Switzerland and other European jurisdictions as part of broader business and investment planning.

Such clients often have legacy ties in the former jurisdiction, including family homes, business operations, bank accounts, investment portfolios, management roles or personal expenditure patterns. At the same time, they may seek residence, treaty access, banking relationships or corporate substance in a new jurisdiction. If the documentary record is inconsistent, the risk is not limited to one tax authority. Information may move between authorities under the applicable international framework.

The practical lesson is that cross-border planning should be approached as an integrated exercise. Legal advice, accounting records, corporate administration, banking disclosures, immigration files, tax-residence representations and correspondence with authorities should be reviewed together. A technically sound structure can still be weakened by careless or inconsistent administrative communications.

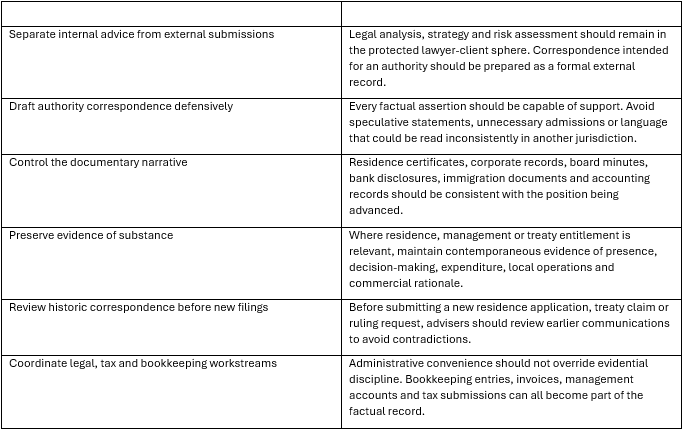

The decision supports a disciplined approach to communications with tax authorities. The following points are not a substitute for jurisdiction-specific advice, but they provide a useful working framework for advisers handling cross-border tax and residence matters.

A balanced reading of the decision is essential. It does not mean that all materials held by lawyers are disclosable. It does not mean that confidential legal advice has lost protection. It does not mean that taxpayers have no procedural rights in administrative assistance proceedings. Nor does it mean that every foreign request will automatically be accepted.

Rather, the decision confirms that the protection of professional secrecy has boundaries. Where correspondence has been sent to a public authority and is held by that authority, the taxpayer should not assume that the lawyer’s involvement will prevent transmission if the relevant administrative-assistance requirements are otherwise satisfied.

For professional advisers, the point is not to avoid engagement with tax authorities. Engagement may be necessary and beneficial. The point is to manage that engagement carefully, with a clear understanding that the external administrative record may later be read by someone other than the immediate recipient.

The Swiss Federal Supreme Court’s decision in 2C_506/2024 is a timely reminder that cross-border tax work is evidential as well as technical. The law may permit a residence claim, treaty position or corporate structure, but that position must be supported by a disciplined documentary record.

The practical rule is straightforward: confidential legal advice should be kept within the lawyer-client relationship, whereas correspondence with tax authorities should be treated as part of the administrative file. In cross-border matters, that file may not remain domestic. It may be transmitted under the applicable exchange-of-information framework.

For internationally mobile individuals, entrepreneurs, business owners and investors, the commercial lesson is equally clear. Tax residence, substance, beneficial ownership and treaty-access positions should be planned, documented and communicated consistently from the outset. In modern tax administration, the correspondence trail can be as important as the legal structure itself.

This article is intended as a general professional information piece for tax, legal, accounting and corporate-service professionals, business owners, entrepreneurs and internationally mobile investors. It does not constitute legal or tax advice. Specific cases should be assessed by reference to the relevant facts, applicable treaty, domestic law and procedural rules.

The Court held that correspondence exchanged between a taxpayer’s lawyers and a Swiss tax authority, once held by that authority as part of its administrative file, could be transmitted in international tax administrative assistance proceedings. The case should be read as a privilege-boundary decision, not as a general rejection of lawyer-client confidentiality.

No. Confidential legal advice, internal legal analysis and communications between lawyer and client remain important protected categories. The decision concerns correspondence submitted to a public authority and held within that authority’s administrative record.

Tax residence disputes often turn on the factual record behind a residence certificate or formal filing. A foreign tax authority may use administrative-assistance mechanisms to test whether statements made to a Swiss authority are consistent with the taxpayer’s actual centre of life, business activity, management role and economic interests.

Advisers should treat correspondence with a tax authority as a formal external record. Factual assertions should be supportable, consistent with other documentation and drafted with the possibility of later cross-border review in mind.

Yes, although the case concerned individual residence. The same evidential discipline is relevant for companies where questions of management, permanent establishment, beneficial ownership, treaty access or economic substance may later be reviewed by another tax authority.

They should keep privileged legal advice separate from external submissions, maintain a consistent factual record, review historic correspondence before new filings, and coordinate tax, legal, accounting, corporate and banking documentation.

Articles are provided for general informational purposes by an authorised corporate services provider and do not constitute legal advice.

Receive updates with practical insights on international business, law, tax, accounting, and compliance.

Be the first to hear about our latest discounts and special offers!

Follow our Telegram channel for offshore industry news:

Want updates by e-mail?

Enter your email address below to subscribe to our newsletter!