Eltoma Corporate Services — Authorised Corporate Services Provider

Articles are provided for general informational purposes by an authorised corporate services provider and do not constitute legal advice.

Incorporating a company has never been easier. In the United Kingdom, an online incorporation is commonly completed within 24 hours. In Hong Kong, electronic certificates for a private company limited by shares are normally issued within one hour. In Singapore, most registrations are approved shortly after payment, although more complex applications can take materially longer. Cyprus also offers an accelerated incorporation procedure for an additional fee.

That speed is precisely why many founders underestimate the true scope of an international business set-up. Incorporation is usually the fastest part of the project. The more difficult work begins when the company must satisfy bank onboarding, payment-provider checks, tax analysis, sanctions screening, investor due diligence or licensing review.

FATF standards require financial institutions to identify and verify the customer and the beneficial owner, understand the purpose and intended nature of the relationship, and decline or terminate the relationship where customer due diligence cannot be completed properly. The legal entity is therefore only the wrapper. The real question is whether the structure can operate credibly in the real world.

This is particularly important in the present transparency environment. The OECD’s Global Forum now brings together 172 jurisdictions, and the 2025 peer review update on the automatic exchange of financial account information covers 118 jurisdictions. Cross-border transparency is no longer an optional feature of the system; it is an integral part of the system.

This is why a “cheap company package” so often becomes merely the first payment in a much larger restructuring project.

The mass market for corporate services is usually optimised around one measurable result: delivering a registered legal entity as quickly as possible. The regulatory and commercial reality is different. A bank does not merely ask whether the company exists. It asks whether the institution can explain who controls the business, where the capital came from, which countries and counterparties will be involved, how revenue will be earned and whether the activity is compatible with its risk appetite.

A company may therefore be validly incorporated yet remain unusable for its intended purpose. It may be unable to obtain an account, unsuitable for its payment flows, misaligned with the owners’ tax position, incapable of supporting a future licence or unprepared for investor due diligence.

The apparent saving at the incorporation stage is then replaced by the cost of a second onboarding, revised KYC submissions, changes to directors or shareholders, contractual re-documentation, relocation of intellectual property, a new banking application, tax analysis or a full regulatory rebuild.

Incorporation does not automatically determine tax residence. HMRC states that a company may be resident where its central management and control actually abides, while Singapore’s IRAS likewise links corporate tax residence to the place where control and management of the business is exercised. A company may therefore be incorporated in one jurisdiction while the underlying facts indicate management in another.

Practical consequence. A nominal registered office, local service provider or incorporation certificate will not, by itself, resolve questions concerning effective management, substance, permanent establishment risk, withholding taxes or the personal reporting obligations of the owners.

Financial institutions and fintech providers do not assess only whether a company legally exists. They must be able to understand who owns and controls it, what it does, where it trades, how it earns revenue, which documents support the activity and whether the ownership and business model fall within their risk appetite.

Airwallex, for example, requires a company to be active, incorporated in an eligible country, outside unsupported industries, and not to constitute a shell bank or bearer-share entity. Its onboarding process may include beneficial ownership information, tax documents and supporting business records. Wise Business similarly requires the business to be registered in a supported country and to maintain a physical trading address in a jurisdiction where the service is available.

Banks have also become more demanding because their own regulatory exposure has become more costly. Nordea publicly states that it may request evidence concerning source of wealth, origin of funds, business relationships and intended use of banking services. The bank has also reported substantial investment in financial-crime controls, a large specialist workforce and the monitoring of billions of transactions. In 2024, Nordea entered into a USD 35 million settlement with the New York State Department of Financial Services in relation to historical AML deficiencies.

Commercial reality. A company can be perfectly valid as a matter of corporate law and nevertheless be unsuitable for a particular bank or payment provider. The payment route should therefore be tested before, rather than after, incorporation.

Modern sanctions compliance extends far beyond checking whether the company’s name appears on a list. In the United Kingdom, OFSI guidance places particular emphasis on ownership and control. In the United States, OFAC’s 50 Percent Rule provides that an entity owned 50 per cent or more, directly or indirectly, by one or more blocked persons is itself treated as blocked, even if it is not separately designated.

The European Union’s sanctions framework likewise requires businesses to understand how active sanctions regimes apply in practice. Accordingly, sanctions analysis must consider direct and indirect ownership, actual control, counterparties, payment routes, goods and services, intermediaries, logistics chains and the broader commercial purpose of the transaction.

Risk point. The absence of a company name from a sanctions list is not conclusive. A bank or counterparty may still decline the relationship because of ownership, control, geography, sector or indirect exposure.

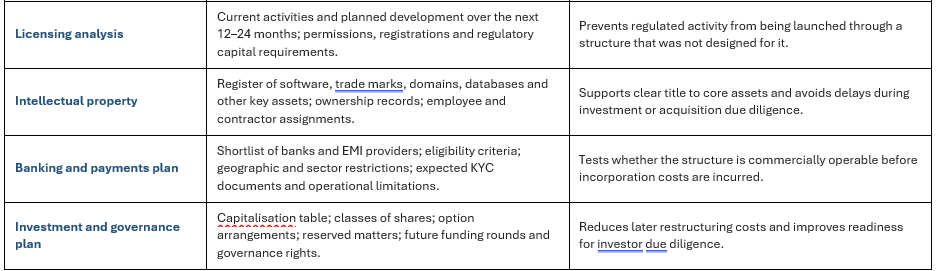

If a business is moving towards payments, electronic money, remittance or another regulated activity, an ordinary trading company may be the wrong starting point. The FCA regulates payment institutions and electronic money institutions in the United Kingdom. MAS issues three categories of licence for payment service providers under Singapore’s Payment Services Act.

The Central Bank of Cyprus states that an electronic money institution must be incorporated in Cyprus, maintain both its registered office and head office there, and conduct at least part of its electronic-money or related payment-services business in Cyprus. In Hong Kong, the money service operator regime includes fit-and-proper assessments, business-plan requirements, AML/CFT policies and scrutiny of the premises used for the business.

Cost of getting it wrong. Where regulated activity has already commenced through an unsuitable structure, the business may have to revise its corporate model, governance, capital, policies, staffing, banking description and contractual arrangements before a licensing application can proceed.

Investor readiness is another common source of hidden cost. WIPO notes that a properly designed intellectual-property strategy can facilitate access to finance and attract investors and commercial partners. The British Business Bank describes the capitalisation table as a key record of the company’s equity ownership, while due diligence depends upon the completeness and accuracy of the information presented.

Where software code, trade marks, domain names or core technology are not owned by the correct company, the issue often emerges at the most commercially sensitive point: during fundraising, an acquisition, a lender review or another form of due diligence.

Due diligence concern. If a founder, contractor or another group company owns a key asset, the operating company may not be able to demonstrate clear title. The resulting corrective work may involve assignments, licences, warranties, tax analysis and revisions to the investment documentation.

The economic problem is not that incorporation services are inexpensive. The problem is that the price of incorporation is often presented as though it were the total price of establishing an international business structure.

In reality, the cost of a workable structure includes owner and sanctions analysis, tax-residence review, banking strategy, KYC preparation, payment-flow modelling, licensing analysis, intellectual-property arrangements, corporate governance and continuing compliance.

When these elements are omitted at the outset, they do not disappear. They re-emerge later, usually when the company is already under commercial pressure to open an account, receive a material payment, complete a funding round or satisfy a regulator.

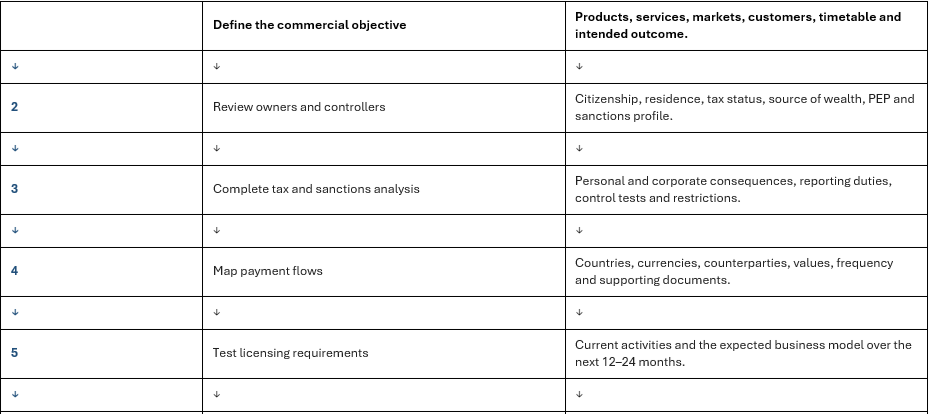

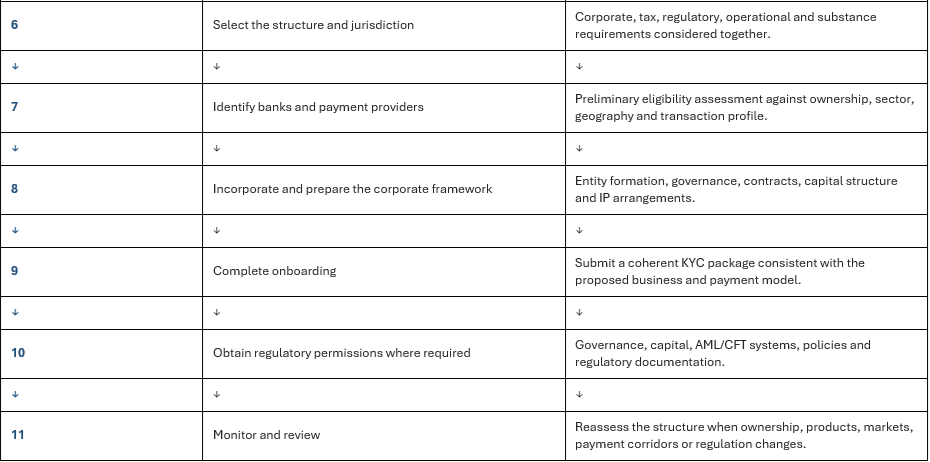

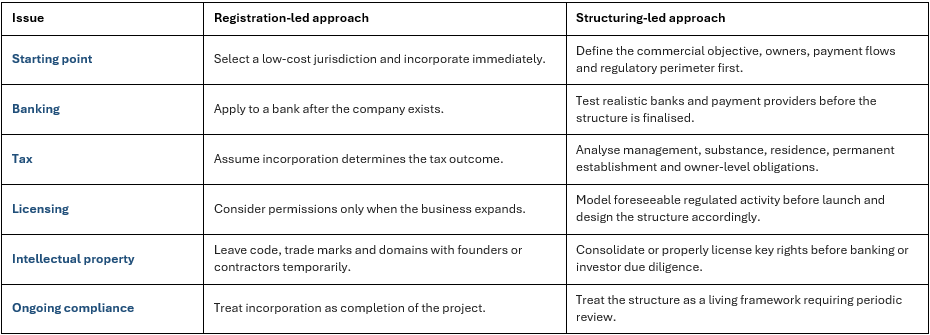

A properly structured project should proceed from the commercial and compliance facts towards the choice of legal entity, rather than beginning with the jurisdiction and attempting to fit the business into it afterwards.

The following information should ordinarily be assembled and reviewed before the jurisdiction and legal form are finalised.

The following sequence reflects how a modern bank, regulator, tax authority or investor is likely to assess the structure. Identity, control, purpose and payment flows should be understood before the corporate wrapper is selected.

This is where experienced structuring advice creates real value. The purpose is not simply to identify where a company can be incorporated. It is to determine how the business will be viewed by a bank, payment provider, tax authority, regulator and investor — not only on the date of incorporation, but one or two years later.

At ELTOMA, that is the practical distinction between registration and structuring. Company formation is a filing exercise. Business structuring is the work of designing a cross-border arrangement that is bankable, operational, regulator-aware, tax-conscious and ready for growth.

A cheap ready-made company may appear efficient on day one. However, if it results in failed onboarding, a tax mismatch, a licensing rebuild or an investor due-diligence problem, it was never genuinely inexpensive. It was simply the first invoice in a more expensive project.

Because the incorporation fee covers only the creation or acquisition of the legal entity. A workable international structure may also require tax-residence analysis, banking preparation, sanctions and AML review, licensing analysis, intellectual-property documentation and ongoing compliance.

No. A bank or payment provider still reviews the owners, controllers, business model, countries, counterparties, source of wealth, source of funds and expected payment flows. A pre-existing company does not remove these checks.

Not by itself. Depending on the relevant law and treaties, corporate residence and permanent-establishment exposure may also depend on where strategic decisions are taken, where management operates and where the business has substance.

The owners and beneficial owners, tax residence, sanctions profile, source of wealth and funds, business model, payment flows, banking options, licensing perimeter, management and substance, intellectual property and future investment plans should be reviewed first.

Yes. Some sanctions regimes extend restrictions to entities owned or controlled by designated persons. Banks and counterparties may also apply broader risk policies based on indirect exposure, sector, geography and transaction routes.

Licensing should be assessed before the business launches the relevant activity. Where the business may move into payments, electronic money, remittance or similar services within the next 12–24 months, the future regulatory model should influence the initial structure.

Investors and lenders expect the company to demonstrate clear ownership or valid licensing of its software, trade marks, domains and other core assets. Missing assignments can delay due diligence and reduce the value or bankability of the business.

At least annually and whenever ownership, management, products, markets, payment corridors, banking arrangements, regulation or sanctions exposure changes.

Articles are provided for general informational purposes by an authorised corporate services provider and do not constitute legal advice.

Receive updates with practical insights on international business, law, tax, accounting, and compliance.

Be the first to hear about our latest discounts and special offers!

Follow our Telegram channel for offshore industry news:

Want updates by e-mail?

Enter your email address below to subscribe to our newsletter!